Republicans push high deductible plans and health savings accounts

Sarah Monroe once had a relatively comfortable middle-class life.

She and her family lived in a neatly landscaped neighborhood near Cleveland. They had a six-figure income and health insurance through her job. Then, four years ago, when Monroe was pregnant with twin girls, something started to feel off.

“I kept having to come into the emergency room for fainting and other symptoms,” recalled Monroe, 43, who works for an insurance company.

The babies were fine. But after months of tests and hospital trips, Monroe was diagnosed with a potentially dangerous heart condition.

It would be costly. Within a year, as she juggled a serious illness and a pair of newborns, Monroe was buried under more than $13,000 in medical debt.

Part of the reason: Like tens of millions of Americans, she had a high-deductible health plan. People with these plans typically pay thousands of dollars out of their own pockets before coverage kicks in.

The plans, which have become common over the past two decades, are getting renewed attention thanks to President Donald Trump and his GOP allies in Congress.

Many Republicans are reluctant to extend government subsidies that help cover patients’ medical bills and insurance premiums through the Affordable Care Act.

And although GOP leaders have yet to coalesce around an alternative, several leading Republican lawmakers have proposed Americans who don’t get insurance through an employer should get cash in a special health care account, paired with a high-deductible health plan.

In such an arrangement, someone could choose a plan on an ACA marketplace that costs less per month but comes with an annual deductible that can top $7,000 for an individual plan.

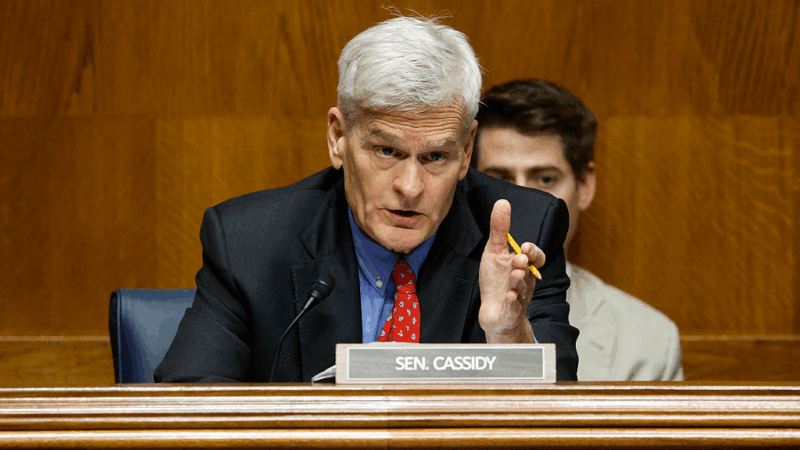

“A patient makes the decision,” Sen. Bill Cassidy, R-La., said at a recent hearing. “It empowers the patient to lower the cost.”

In a post on Truth Social last month, Trump said: “The only healthcare I will support or approve is sending the money directly back to the people.”

“Skin in the game”

Conservative economists and GOP lawmakers have been making similar arguments since high-deductible health plans started to catch on two decades ago.

Back then, a backlash against the limitations of HMOs, or health maintenance organizations, propelled many employers to move workers into these plans, which were supposed to empower patients and control costs. A change in tax law allowed patients in these plans to put away money in tax-free health savings accounts to cover medical bills.

“The notion was that if a consumer has ‘skin in the game,’ they will be more likely to seek higher-quality, lower-cost care,” said Shawn Gremminger, who leads the National Alliance of Healthcare Purchaser Coalitions, a nonprofit that works with employers that offer their workers health benefits.

“The unfortunate reality is that largely has not been the case,” Gremminger said.

Today, nearly all health plans comes with a deductible, with the average for a single worker with job-based coverage approaching $1,700, up from around $300 in 2006.

Plans with deductibles that exceed $1,650 can be paired with a tax-free health savings account.

But even as deductibles became widespread over the last 20 years, medical prices in the U.S. skyrocketed. The average price of a knee replacement, for example, increased 74% from 2003 to 2016, more than double the rate of overall inflation.

At the same time, patients have been left with thousands of dollars of medical bills they can’t pay, despite having health insurance.

About 100 million people in the U.S. have some form of health care debt, a 2022 survey showed.

Most, like Monroe, are insured.

Medical price shopping isn’t easy

Although Monroe had a health savings account paired with her high-deductible plan, she was never able to save more than a few thousand dollars, she said. That wasn’t nearly enough to cover the big bills when her twins were born and when she got really ill.

“It’s impossible, I will tell you, impossible to pay medical bills,” she said.

There was another problem with her high-deductible plan. Although these plans are supposed to encourage patients to shop around for medical care to find the lowest prices, Monroe found this impractical when she had a complex pregnancy and heart troubles.

Instead, Monroe chose the largest health system in her area.

“I went with that one as far as medical risk,” she said. “If anything were to happen, I could then be transferred within that system.”

Federal rules that require hospitals to post more of their prices can make comparing institutions easier than it used to be.

But unlike a car or a computer, most medical services remain difficult to shop for, in part because they stem from an emergency or are complex and can stretch over numerous years.

Researchers at the nonprofit Health Care Cost Institute, for example, estimated that just 7% of total health care spending for Americans with job-based coverage was for services that realistically could be shopped for.

Fumiko Chino, an oncologist at the MD Anderson Cancer Center in Houston, said it makes no sense to expect patients with cancer or another chronic disease to go out and compare prices for complicated medical care such as surgeries, radiation, or chemotherapy after they’ve been diagnosed with a potentially deadly illness.

“You’re not going be able to actually do that effectively,” Chino said, “and certainly not within the time frame that you would need to when facing a cancer diagnosis and the imminent need to start treatment.”

Drowning in bills

Chino said patients with high deductibles are often instead slammed with a flood of huge medical bills that lead to debt and a cascade of other problems.

She and other researchers found in a study of more than 8,000 cancer patients presented last year at the American Society of Clinical Oncology that cancer patients who had high-deductible health insurance were more likely to die than similar patients without that kind of coverage.

For her part, Monroe and her family were forced to move out of their house and into a 1,100-square-foot apartment.

She drained her savings. Her credit score sank. And her car was repossessed.

There have been other sacrifices, too. “When families get to have nice Christmases or get to go on spring break,” Monroe said, hers often does not.

She is thankful that her children are healthy. And she continues to have a job. But Monroe said she can’t imagine why anyone would want to double down on the high-deductible model for health care.

“We owe it to ourselves to do it a different way,” she said. “We can’t treat people like this.”

KFF Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at KFF.

Trump says he is ‘not happy’ with the Iran nuclear talks but indicates he’ll give them more time

U.S. President Donald Trump said Friday he's "not happy" with the latest talks over Iran's nuclear program but indicated he would give negotiators more time to reach a deal to avert another war in the Middle East.

Bill Clinton says he ‘did nothing wrong’ with Epstein as he faced grilling over their relationship

Former President Bill Clinton told members of Congress on Friday that he "did nothing wrong" in his relationship with Jeffrey Epstein and saw no signs of Epstein's sexual abuse as he faced hours of grilling from lawmakers over his connections to the disgraced financier from more than two decades ago.

Pentagon puts Scouts ‘on notice’ over DEI and girl-centered policies

After threatening to sever ties with the organization formerly known as the Boy Scouts, Defense Secretary Hegseth announced a 6-month reprieve

President Trump bans Anthropic from use in government systems

Trump called the AI lab a "RADICAL LEFT, WOKE COMPANY" in a social media post. The Pentagon also ordered all military contractors to stop doing business with Anthropic.

HUD proposes time limits and work requirements for rental aid

The rule would allow housing agencies and landlords to impose such requirements "to encourage self-sufficiency." Critics say most who can work already do, but their wages are low.

Paramount and Warner Bros’ deal is about merging studios, and a whole lot more

The nearly $111 billion marriage would unite Paramount and Warner film studios, streamers and television properties — including CNN — under the control of the wealthy Ellison family.